TriathlonPartnersTV: RILAs Unpacked: Understanding Buffers and Caps

By ira October 02, 2024

RILAs Explained: Buffers and Caps

In this episode of Triathlon PartnersTV, we delve into RILAs, or Registered Indexed Linked Annuities. RILAs are structured investment products whose returns depend on the performance of underlying market indices like the S&P 500 or NASDAQ 100. Each investment structure, referred to as a segment, offers protection against losses through a mechanism known as a buffer. Buffers can protect against the first 10%, 15%, or 20% of losses in the underlying index.

For example, a segment with a 10% buffer will not lose any value if the underlying index declines by 5%. However, if the index falls by 14%, the segment will lose 4%. Buffers operate consistently across different segment types.

In exchange for this protection, each segment has a maximum return limit known as a cap. The cap level is influenced by various factors, including the buffer (with larger buffers resulting in lower caps), interest rates, and market volatility.

Types of Segments

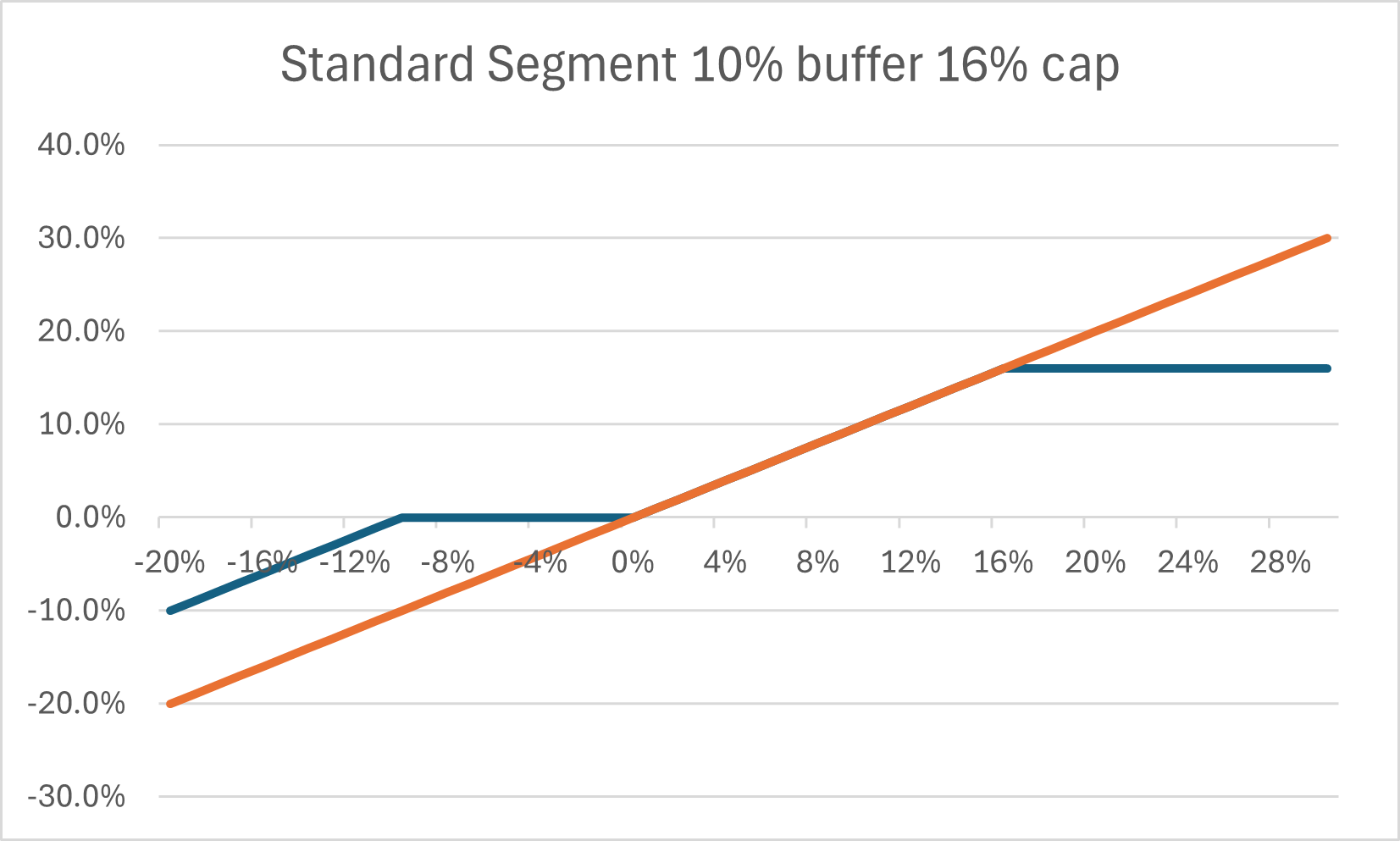

Standard Segment: Mirrors the underlying index performance up to the cap. For example, if the cap is 16%, that is the maximum return of the segment.

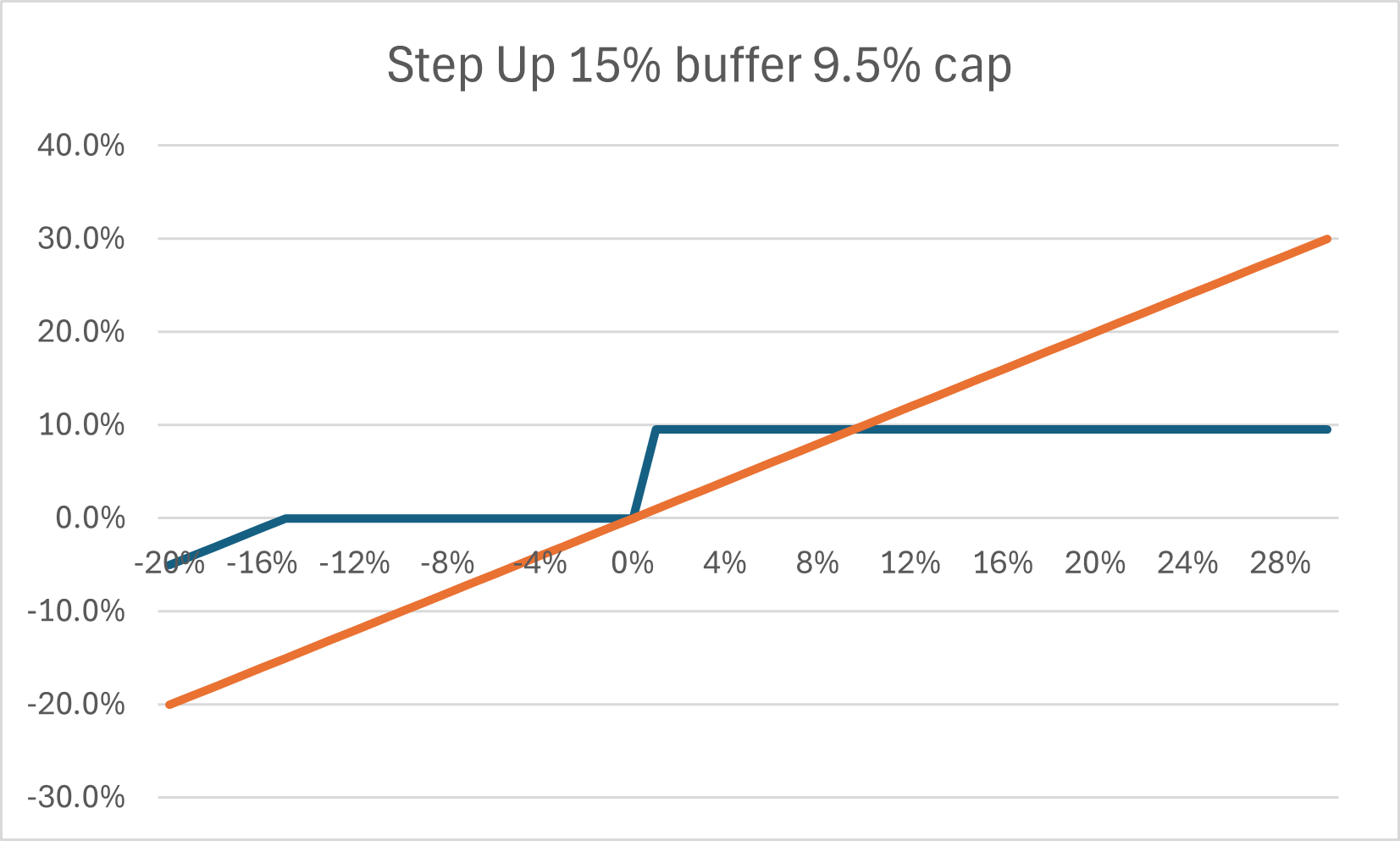

Step Up Segment: If the underlying index is positive, the segment returns the cap. For example, if the cap is 9.5%, it will return this amount as long as the index is positive.

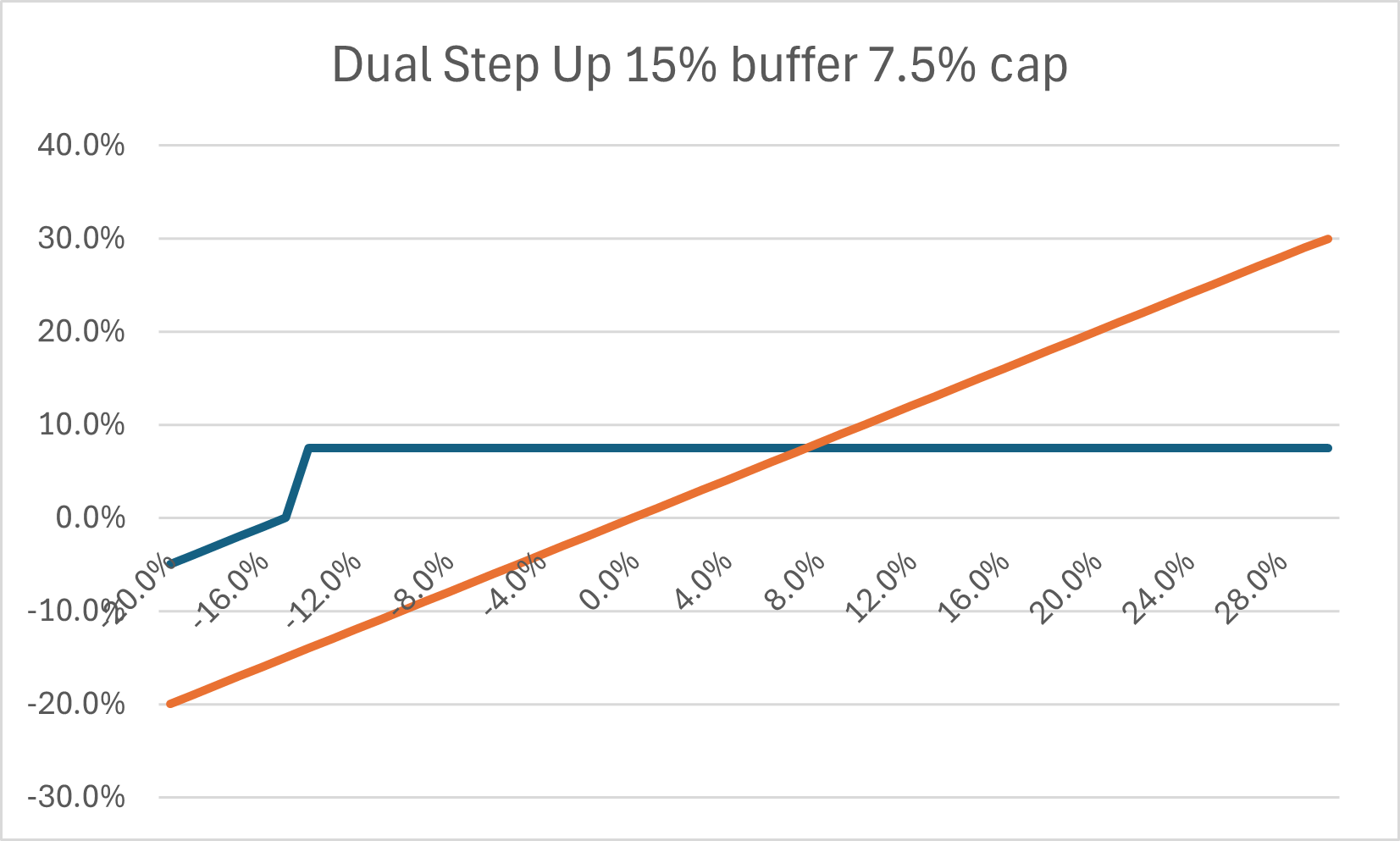

Dual Step Up Segment: This segment returns the cap as long as the index closes above the buffer. For example, with a 15% buffer and a 7.5% cap, it returns 7.5% if the index is above -15%.

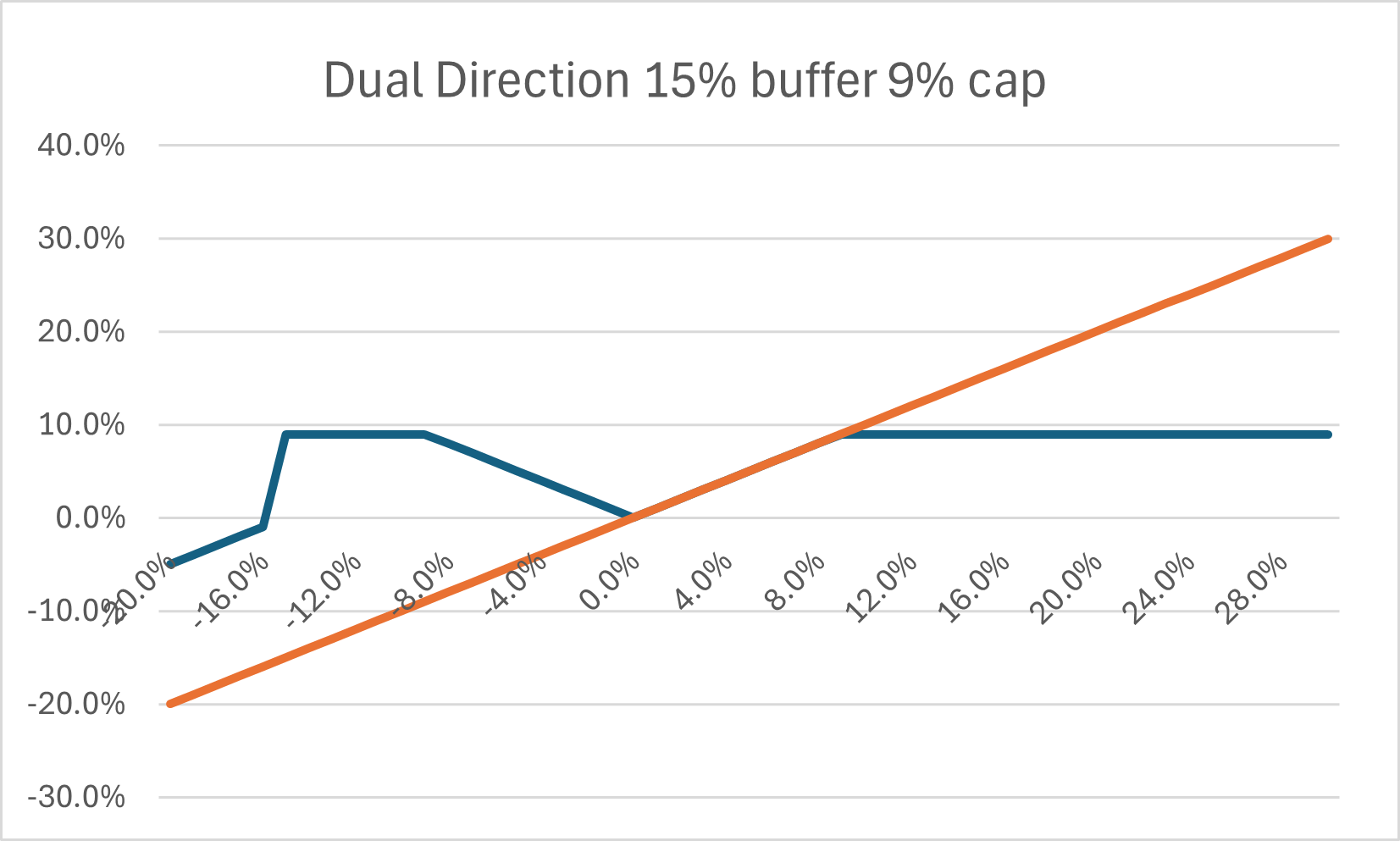

Dual Direction Segment: Combines features of the Standard and Dual Step Up segments. It returns the absolute value of the index return, capped at the maximum. For example, a dual direction segment with a 15% buffer and a 9% cap will pay up to 9% regardless of whether the index rises or falls, until it falls below the buffer level.

Importance of RILAs, Buffers, and Caps

Significantly lower the volatility of your investment portfolio.

Limit the size and number of negative returns. For instance, a market that is up 20% one year and down 20% the next has an average return of 0%, but a real return of -4%. A $100 investment that gains 20% to $120, followed by a 20% loss, ends up at $96.

Annual resets maximize positive returns and minimize down years. If you invested in a segment with a 10% buffer and a 16% cap, you would gain 16% in the first year and lose 10% in the second, resulting in a total of $104.40 after two years.

RILAs can have optional riders (for an additional annual cost) that address other financial goals, including income generation with guaranteed minimum returns, benefits for long-term care expenses, and features for estate planning that return the total initial investment under specific conditions.

Blending Segments to Smooth Returns

The illustrations above demonstrate that each segment offers unique return profiles. The true power of RILAs lies in blending these segments to create a more defined return profile.

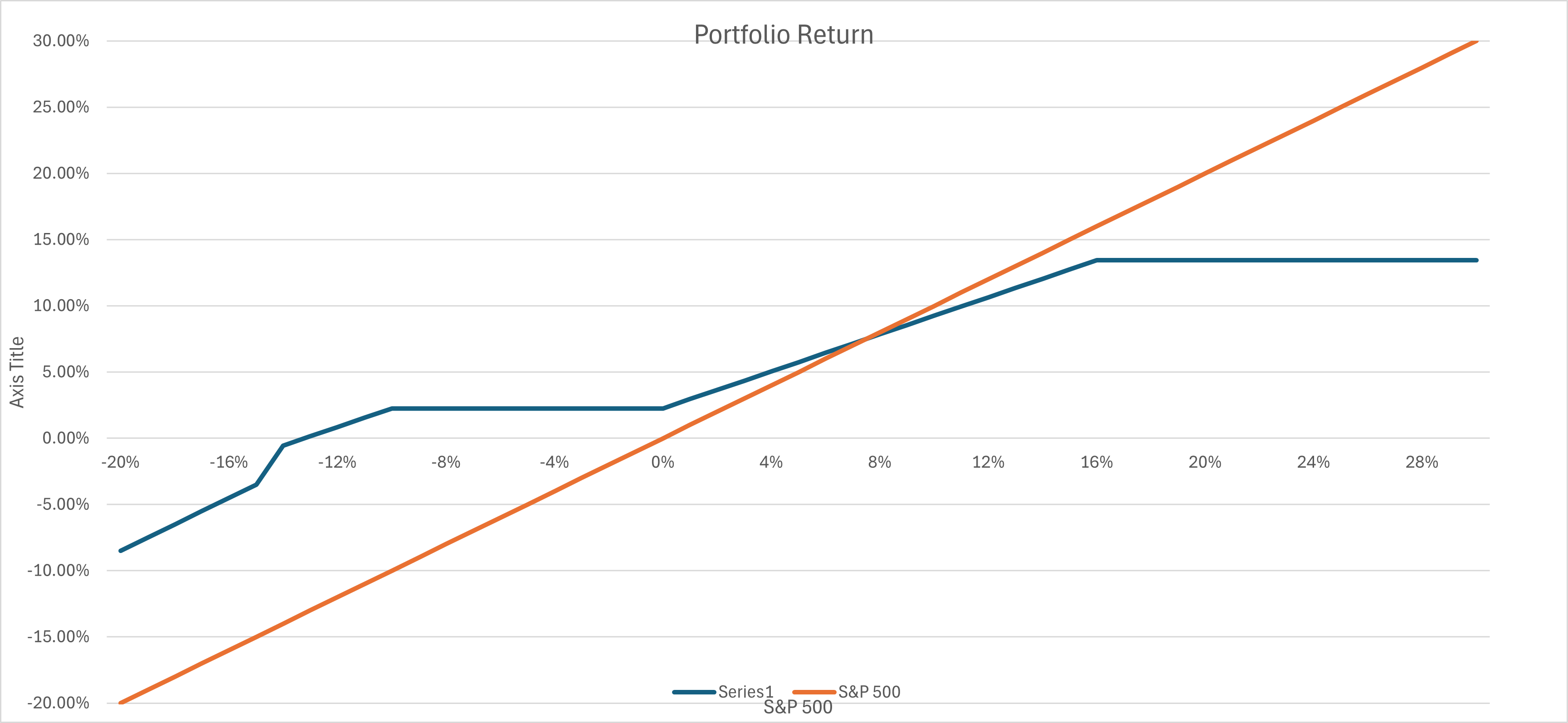

The graph below illustrates a mix of 70% Standard Segment and 30% Dual Step Up Segment. This combination results in a portfolio that returns 2.25% when the index is down between 0% and 10%. It avoids negative returns until the index falls below 13%, and for movements larger than -15%, the RILAs provide protection up to 11.5%.

The cap for this combination is set at 13.45%. This strategy is ideal for soon-to-be retirees who cannot afford market corrections that could delay their retirement plans but still seek modest appreciation to keep up with inflation. The cap offers ample opportunities to achieve above-average returns.

These innovative annuities not only safeguard your savings but also provide annual increases in the amount used to calculate your future income, helping keep your retirement plan on track, regardless of market fluctuations.

Our mission is to engage, educate, and empower you to make informed decisions that align with your retirement goals. We are sincerely grateful to our S.TU.F.F. community—thank you to our Subscribers, Thumbs Up supporters, Followers, and Friends!

By ira

October 02, 2024

By ira

October 02, 2024